In today’s competitive marketplace, many entrepreneurs have successfully built and run their businesses. However, as they enter new phases such as acquiring projects, diversifying, and attracting investors, they often face challenges due to a lack of proper data for decision-making. Frequently, financial records from the beginning of their journey are kept in disorganized Excel worksheets.

Have you experienced this scenario? For instance:

- Invoices are created in MS Word and listed in an Excel sheet, with payments tracked against bank statements.

- Payments are made from both company and personal accounts without proper documentation.

- Post-dated cheques are issued for lease and EMI payments without detailed records.

- Cash withdrawals for personal use are mixed with business transactions.

- Payroll liabilities are paid through bank and petty cash, recorded in separate sheets without adjusting for salary advances.

- Money is transferred to related companies without proper documentation.

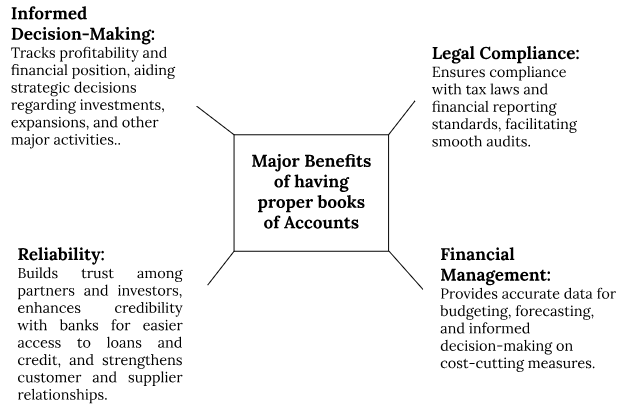

Many entrepreneurs have a mental picture of their profitability and financial position, even if it’s not formally organized. While they focus on growing their business, setting up a proper system for tracking profitability and financial health often takes a backseat. Eventually, they realize the need for maintaining proper books of accounts and documentation.

How the emerging Entrepreneurs Can Overcome These Obstacles:

1. Hire an Accounting Professional:

Depending on the volume of transactions, consider hiring an accountant early in the startup phase. The cost benefits of having a professional can outweigh the expenses.

2. Establish a Workflow Structure:

Design a proper organizational workflow and assign responsibilities aligned with the company’s growth.

3. Use Cloud-Based Accounting Software:

Opt for user-friendly accounting softwares like QuickBooks Online, Zoho Books, or Xero. These softwares help to manage finances efficiently and interpret results easily.

4. Analyze Financial Statements:

Regularly review financial statements to compare results with industry benchmarks and plan budgets for future growth.

If you’re still struggling with incomplete records, consult an accounting and finance professional to reconcile these records and maintain proper books of accounts and documentation.